Wow! I stumbled into Solana tooling last year while chasing a weird NFT bug. My first impression was speed, raw speed, and some chaos. Initially I thought that all explorers were basically interchangeable, but then I spent a week tracing failed transactions and token mint histories and realized the tooling differences actually matter a lot. Here’s what bugs me about many UIs: they hide the gritty data, somethin’ important.

Really? Sol transactions are deceptively simple on the surface, especially for new users. You click send, pay a tiny fee, and the ledger updates fast. But when things go wrong — a duplicate signature, a program failure, an account rent exemption hiccup — the only way to untangle what happened is a good explorer that shows instruction-level details, inner instructions, and account state changes. That level of traceability is what makes NFT tracker tools so valuable.

Hmm… I’ve used a bunch — and yes, I’m biased toward ones that give raw logs. The typical workflow for me is: submit, watch for confirmation, then deep-dive if something’s off. Initially I thought automated scanners would catch every issue, but then I realized that on-chain debugging needs human intuition—reading stack traces, comparing pre- and post-account states, and correlating those with NFT metadata updates to spot mis-mints or rug-prices. Those correlations are why NFT tracker features are not optional for serious collectors.

Here’s the thing. A solid explorer shows you the block, the transaction, and the minutiae in between — it’s very very useful. When I worked on a marketplace incident last fall, I had to manually follow a token transfer across multiple program invocations, check associated token accounts, and then reconstruct the authority chain because the front-end had cached a stale owner — it took hours, but the explorer’s inner instruction trace was the clue that unlocked everything. That kind of forensic work is satisfying, but it can also be maddening. Tools that combine transaction inspection with NFT-centric views — like ownership timelines, metadata mutation logs, and marketplace sale links — dramatically cut investigation time, though building those views requires careful indexing and access to validated metadata sources.

Tool pick

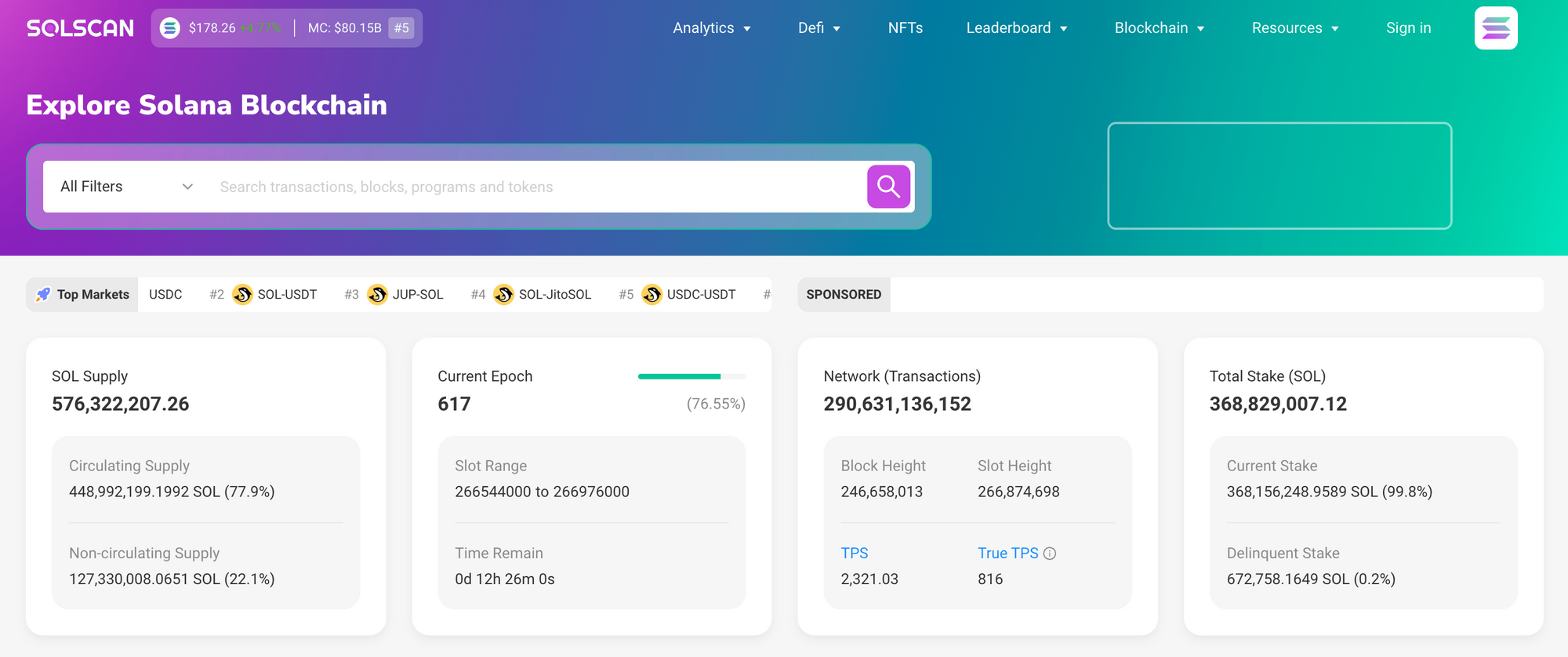

Whoa! Okay, so check this out—I’ve grown to trust explorers that surface inner instructions and return logs verbatim. My instinct said those were optional, but repeated debugging proved otherwise. Initially I thought on-chain explorers were purely read-only conveniences, but after correlating RPC node responses, archival indexer outputs, and a third-party NFT metadata cache I had to re-evaluate that stance because read-only still needs fidelity to be trustworthy. If you’re building an NFT tracker, pick tools with raw traces and timelines. Seriously? Quick FAQ: pick an explorer that exposes inner instructions and raw logs. If you only rely on the transaction summary, you might miss program-level failures and inner transfers that affect NFT ownership, which is why forensic-grade explorers index inner instructions alongside account snapshots. Also verify RPC responsiveness and cluster confirmation counts before trusting stale views. If you want a pragmatic starting point, try a well-maintained explorer like the solscan explorer official site which I lean on frequently because it balances performance with deep inspection features.